Français

Français

🔎 Sunseed prices have further upward potential in 2024/25.

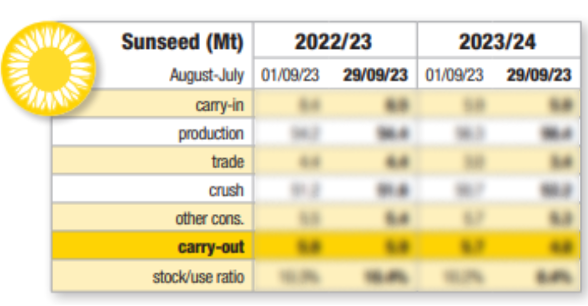

Sunseed production

In France, sunflower plantlet establishment suffered from excessive rainfall, as well as from bird and slug attacks. Some fields need to be reseeded, as conditions permit.

Cool, wet conditions from the second half of April onwards significantly slowed the progress of planting operations in central Spain (Castile and León). In Andalusia, flowering was underway at the end of May. The condition of the sunflower fields remained satisfactory, but a return of rain would be welcome.

Planting was completed in good conditions in Hungary, Romania, and Bulgaria. Sunflower fields will benefit from the good soil water reserves before summer.

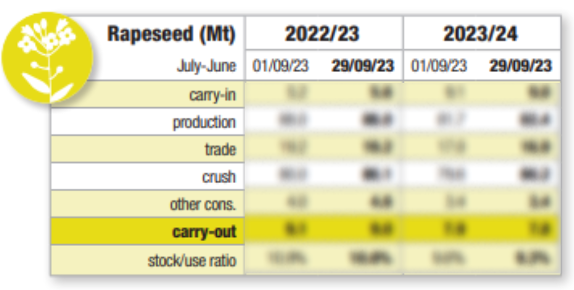

The EU sunflower acreage is revised down very slightly but is still expected to be higher than in 2023/24. The acreage is revised down in France (-40 kha) but revised up in Hungary (+30 kha). Thus, our EU sunseed production forecast is adjusted slightly down to 10.72 Mt.

Sunseed balances

In 2023/24, crushing has been revised up in Ukraine and Russia considering the higher-than-expected oil exporting statistics. As a result, we have raised our estimate for production in Ukraine.

In the EU, the demand for crushing has also increased, based on FEDIOL statistics, while in Turkey it has decreased due to lower imports.

World stocks are revised down, notably in Russia and the EU, with a significant decrease forecast by the end of July 2024. The world sunseed situation looks tight at the end of July 2024. The balance sheet is in deficit in Ukraine, the EU, and Turkey, while the Russian balance sheet shows only a slight surplus.

In the 2024/25 marketing year, despite a downward revision of the aggregate supply, industrial demand is upped slightly in Ukraine and Russia, in line with adjustments made in 2023/24. Crushing is expected down sharply in both countries due to their lower availabilities.

Similarly, in Argentina, a lower industrial demand is forecast due to reduced carry-in stocks. Meanwhile, demand is expected up in the EU-27 and Turkey due to a better harvest expected.

Overall, world crushing is set to fall by 1%, mainly due to lower carry-in stocks, although that decline is limited by robust demand for sunseed oil.

Average prices expected up in new marketing year

In view of the tightness on the EU balance sheet at the end of 2023/24, we estimate that sunseed prices still have a further minor upward potential upward.

In the new marketing year, we are increasing our forecast for average prices as a result of the further downward adjustment in stocks expected at the end of 2024/25.

This is an extract of the World Oilseed Report✂️

Get in touch to leverage full forecasts.