Français

Français

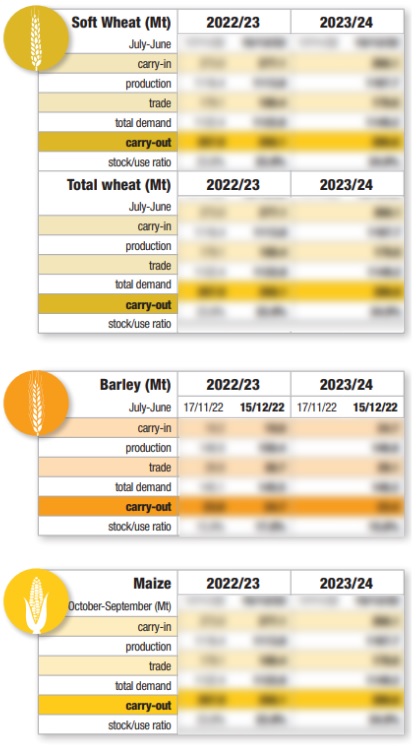

Diminishing harvest potentials in various production zones around the world reduce expected ending stocks in 2023/24, without bringing tightness to markets.

After a period of decline until early June, cereal prices have now started to rise. The weather market is staging a comeback, with 2023/24 harvest forecasts revised lower in various parts of the world. For wheat and barley, production is confirmed at low levels in Spain and North Africa, whilst drought is starting to take hold across northern Europe, affecting yield potentials.

Harvest outlooks in Russia offer a starker contrast, with yield potentials for winter wheat relatively good in the country’s western regions, but arduous sowing conditions for spring wheat in the centre, where conditions are overly dry. This is also the case in Kazakhstan.

In North America, winter wheat production is still expected to be low, whilst conditions for spring wheat plantings/establishment are not ideal.

In Australia, the now confirmed arrival of a potentially fierce weather phenomenon, as early as this summer, should negatively impact yields. But although world wheat production is now expected to fall short of the level of 2022/23, it should still exceed the 5-year average.

Meanwhile, we continue to forecast that world corn production will significantly increase year-on-year, despite less-than-ideal planting conditions in several countries.

Plantings took place much later than usual in Europe, whilst planting progress in Russia was slowed by rains.

In the USA, a lack of rainfall since the start of plantings is already evidenced by the latest USDA crop ratings. Rains will need to return in force between now and late June in order to avoid yield potentials slipping further.