Français

Français🔎 Wheat and barley stocks expected to remain high in Ukraine and Russia in 2023/24 in a tight world market overall – return to good equilibrium on world corn market still in sight.

Bearish price pressure from Russian wheat

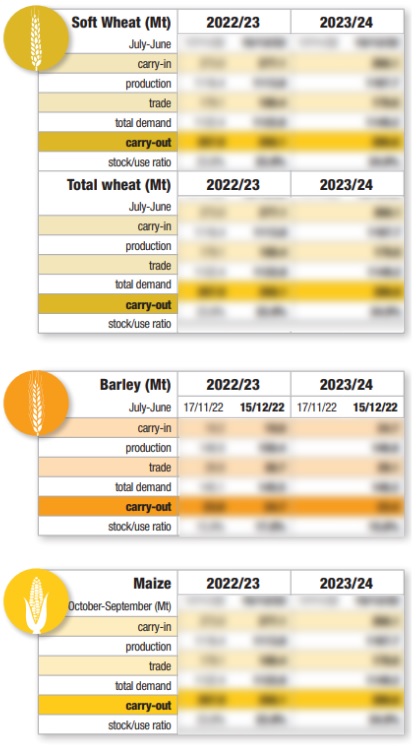

Russia continues to make its mark on world grain markets. Although smaller than the all-time highs of 2022, the wheat and barley harvests in Russia look set to exceed expectations, with the wheat harvest projected to be the second largest ever.

At the same time, Russia has exported enormous quantities of wheat and barley since the start of the new marketing year, reflecting its good harvest and large carryover stocks. Russian wheat is the most competitive on the world market and is creating bearish price pressure for the other origins. Russia’s influence on the wheat and barley markets is accentuated following this month’s reduced harvest forecasts for Canada and Australia.

These origins will thus account for smaller shares of world trade in 2023/24 than previously anticipated. Russian wheat could still compete for market share with European (EU27) origins, but the latter have made a rather sluggish start to the export campaign and are less competitive. The prices of EU wheat origins will need to fall closer to the Russian wheat price before any significant surge in EU exports could be expected.

Brazilian corn is more competitive than its US rival

Meanwhile, record quantities of Brazilian corn are arriving onto the world market. Brazil’s safrinha harvest has reached an all-time high this season and Brazilian corn is more competitive than its US rival – although American corn is certainly attracting its fair share of attention with the harvest just beginning.

US harvest outcomes remain uncertain at this stage: growing areas are very large for the 2023 harvest, but during the growing cycle the crops were hit by high temperatures and lack of water on several occasions. At present, we anticipate a substantial year-on-year production increase, despite lower estimated yields.

Ukrainian exports

The grain markets also find themselves rather dependent on the situation in Ukraine. Russian bombardments have again targeted the Ukrainian Danube ports of Reni and Izmail since last month, pushing up logistical costs for shippers seeking to export grain from these ports.

Ukrainian exports were slightly lower in August 2023 than in August 2022, when the secure maritime corridor had only just started to operate. Ukraine apparently exported 2.4 Mt of cereals in August 2023, and a total of 4.7 Mt since July 1, 2023. Our forecast for Ukrainian exports for the three cereals combined is based on a rate of around 2.7 Mt for each month during the remainder of the campaign.

Tight world cereal market

➡️ Wheat – We continue to forecast a relatively tight world wheat market in 2023/24, although there a stark contrast exists between outlooks for the different regions of the world.

The situation is reminiscent of marketing year 2022/23, with global world wheat stocks concentrated mainly in Russia and Ukraine, and equilibrium on the EU27 market. By contrast, the outlook is very tight for North America, and relatively tight for Australia.

➡️ Barley – A similar geographical contrast exists, although in contrast to the wheat market, the outlook for barley is tighter overall.

➡️ Corn – World corn market is still on course to return to equilibrium in 2023/24. These balance sheet projections are based on moderately rebounding animal sector demand and human/industrial demand, against the backdrop of a still sluggish (though recovering) global economy.

Price movements

In terms of pricing, we forecast that Russian wheat prices will decrease very slightly from the current level, given the high projected volume of stocks in Russia.

West European wheat prices could fall more sharply, to close the gap with Russian wheat.

Russian barley, thus far extremely competitive, could see its price edge higher as the campaign unfolds, whilst west EU barley prices could fall more sharply amid the bearish influence of wheat.

Meanwhile, we also think that US corn prices will fall compared with current levels.

Grain prices would likely have a greater downside potential if Russia’s harvest turned out larger than currently expected, whilst conversely, prices could still rebound if Australia’s wheat and/or barley harvests turned out lower than expected, or the US corn harvest ended in disappointment.